Chiki Shimbunsha Co., Ltd. (TSE Standard: 2164), the listed regional newspaper publisher, is activating its takeover-defense policy against seven shareholders whose combined stake has reached 30.95% of voting rights. The board voted unanimously on 13 July 2026, following a unanimous recommendation from its independent committee, that MTM Capital Co., Ltd., Option House Co., Ltd., Trading One LLC, Keisuke Yagi, Choiz Co., Ltd., B.R.B. Partners Co., Ltd. and Takeshi Sagara had acted in concert and had not complied with the company's defense policy.

Dilution, but only for the target

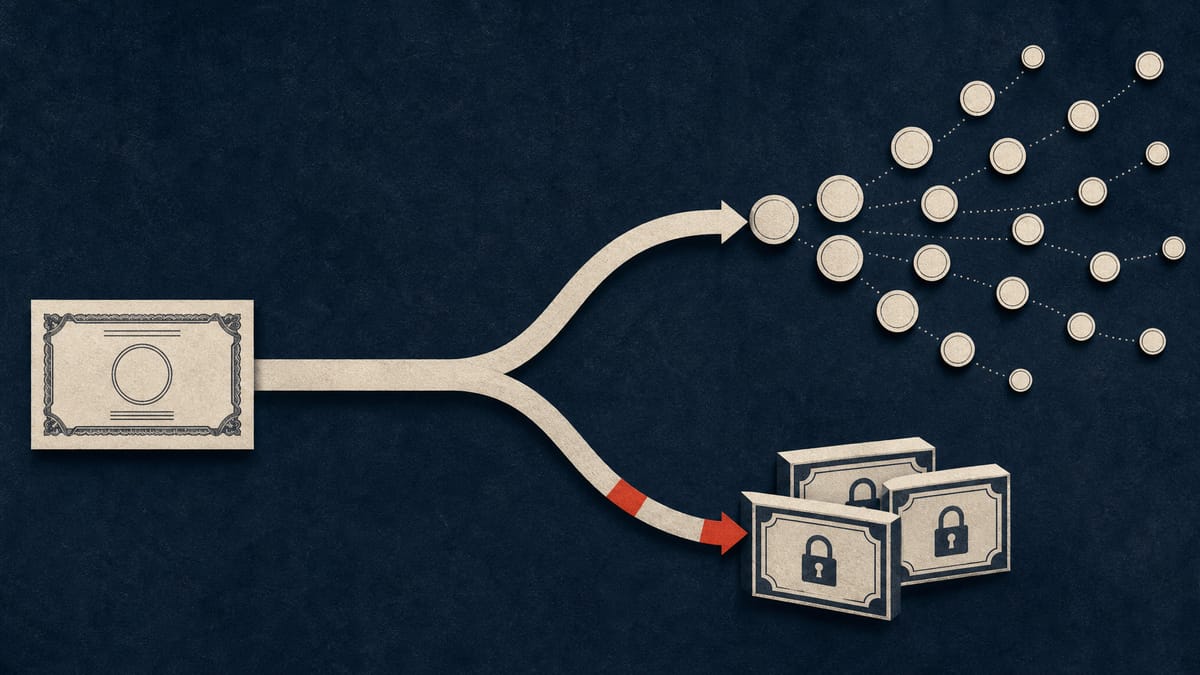

The mechanism is a classic poison pill. Chiki Shimbunsha will issue its 12th Series A stock acquisition rights, free of charge, to every shareholder on the register as of 10 August 2026. On 27 August 2026, it plans to buy those rights back under a discriminatory acquisition clause. Ordinary shareholders will be paid in common stock for their rights. The seven named holders, along with securities firms and margin lenders handling positions tied to them, will instead receive restricted Series B rights rather than tradeable shares. The practical effect is to shrink the target group's economic and voting stake while leaving other shareholders roughly where they started.

A repeat performance

This is not the company's first move this year. In January 2026, the board identified a separate shareholder group it suspected of holding stock through margin-trading positions rather than in its own name, a structure that can make a real stake harder to see on the shareholder register. The company later carried out a stock split at a ratio of 1.8 shares for every share held, effective 26 June 2026, a move partly intended to force such holders to convert margin positions into shares they must register in their own name.

Shareholders get the final word, eventually

Because the company is acting before putting the matter to a shareholder vote, it plans to seek approval after the fact. The board intends to place a ratification proposal before the 42nd annual general meeting, expected around November 2026. If shareholders decline to ratify the defense, the company has said it will act to restore the position to what it would have been had the measure never been triggered. Until that meeting, the arithmetic of who ends up holding tradeable shares and who ends up holding restricted rights will already have been settled.